Digital payments have become an indispensable part of everyday life, but just because they are digital, doesn’t mean they are all equally innovative. Many of the world’s biggest digital payment services like Alipay, Paypal or Apple Pay function more or less like traditional payment providers Visa or Mastercard in that they advance payments for their customers and take the money out of their accounts later.

While innovation for these providers is mostly limited to usability and integration, for example into smartphone use, innovation focused on actual payment processing happens outside the limelight.

Real-time payments – the near-immediate transfer of funds from one bank account to another – is one such example. As data from ACI Worldwide shows, 9.8 percent of global electronic transaction were already done in real time in 2020.

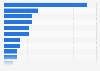

India was the country with the highest real-time transaction value at $25.5 billion, followed by $15.7 billion in China and $6 billion in South Korea. Thailand beats the UK in real time payments, ahead of Nigeria in rank 6.

Developed and developing countries mix among the places which use real-time payments most often, showing that countries with less developed payment infrastructures can prove more innovative in payment solutions. South Asia and Sub-Saharan Africa are also the regions where another payment innovation, mobile money – the use of mobile phone accounts instead of bank accounts - has been thriving most.

In India, the government has been overseeing real time payments since their implementation in 2010, much earlier than in most other countries. The system is currently supported by more than 200 banks. In the U.S., payment service Venmo facilitates instant payments but charges a fee, while regular transfers that take one to three business days are free on the app.