In developed and emerging economies, national debt burdens have increase majorly during the last decades as seen in IMF data. As our graphic shows, some countries were quicker than others to pile on the debt, but debt growth outpacing GDP growth is a common thread for many nations.

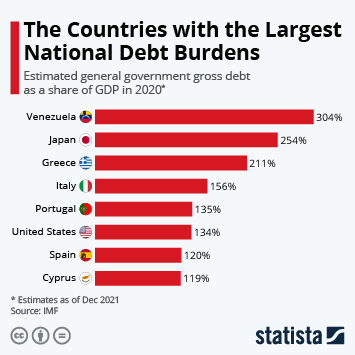

With economic development having been speedy in the country, China stands out for exceptionally fast debt growth during the time period. Yet, at a 68 percent debt-to-GDP ratio, the country is far from being among the nations with the highest debt levels. The top 5 of the countries with the highest relative debt in 2020 consisted of Venezuela, Japan, Greece, Italy and Portugal, with the United States following promptly in rank 6 (of the 87 countries where data was available). A more comprehensive, but less up-to-date list shows the country 12th out of 186 nations in 2015.

While conventional wisdom sees debt that grows faster than GDP as a threat to the future (when debt servicing and interest become an ever-growing burden), the lack of economic contractions many countries had seen between 2009 and 2020 had many believe that the growing debt wasn’t so bad after all. After the coronavirus shocked the global economy, inflation-reducing measures are raising debt servicing costs and the war in Ukraine has thrown world markets into disarray once more, mounting debt might once more seem like a challenge. Additionally, economists believed even before the recent crises that outsized debt burdens hamper the productivity of economies and actually weaken the growth that happens during periods of expansion.

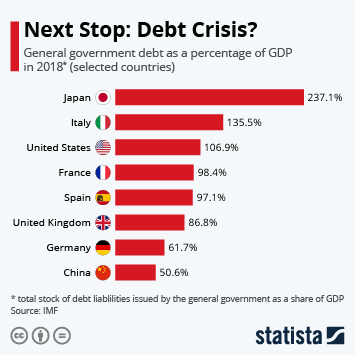

Adverse events have historically caused countries to take on debt more quickly, as illustrated by the examples of Japan and Greece. Both countries experienced additional crises – the 1990 assets bubble and the Euro stability crisis, respectively – which caused their national debts to balloon even more than elsewhere. The latter crisis also affected debt levels in Italy, Portugal and Spain.