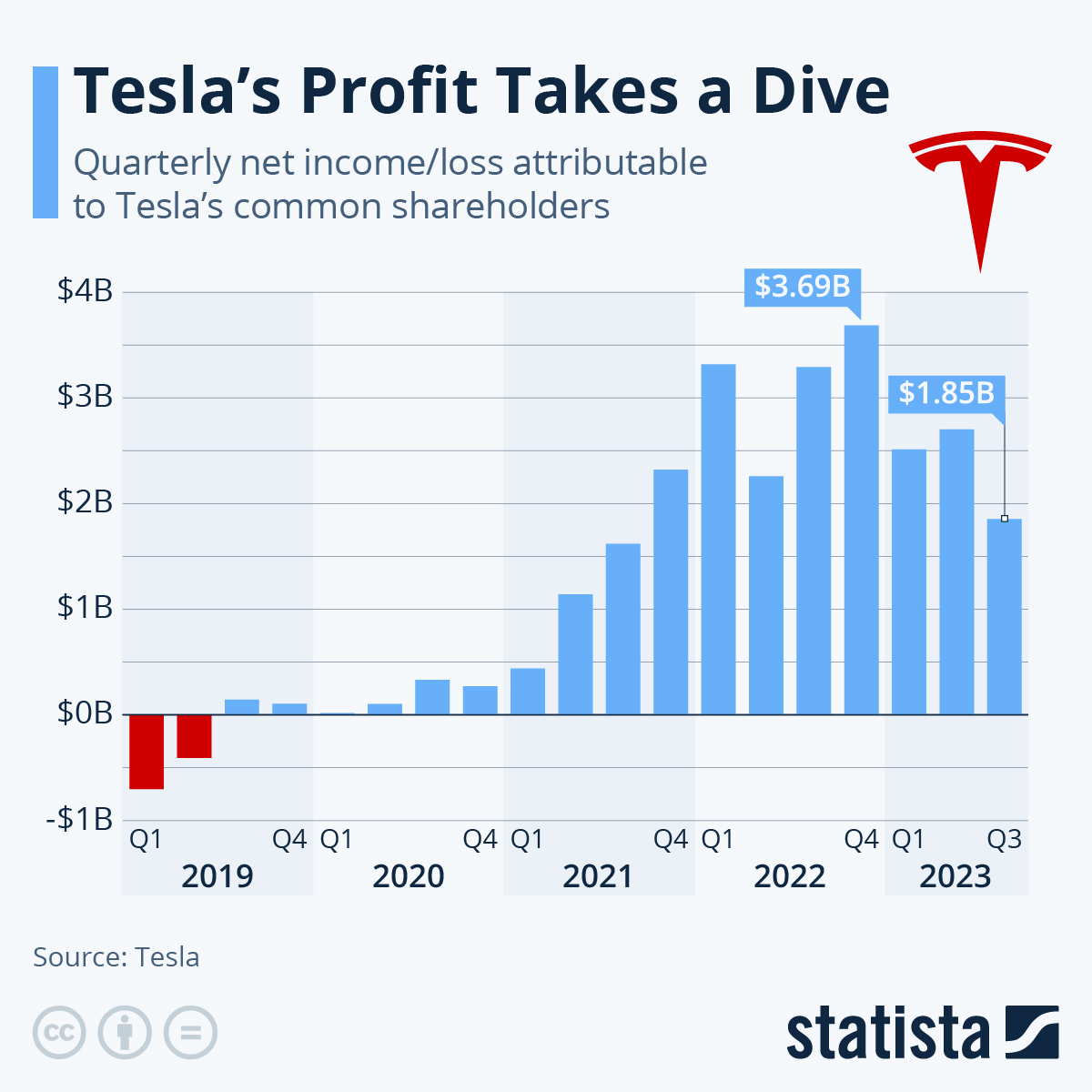

When Tesla finally joined the S&P 500 index in December 2020, the profitability criterion - an eligible company's most recent quarter’s earnings and the sum of its trailing four consecutive quarters’ earnings must be positive - was the last box to be checked by the electric car maker. And while Tesla had a history of loss-making, even bringing it "within single-digit weeks" of bankruptcy in 2018, according to CEO Elon Musk, those days had appeared to be in the past. Up to the end of 2022, the company had posted a bottom line which was largely going in the right direction.

Generating profit in 2023, however, has proved a far more challenging task for the company which posted multiple record quarters throughout the pandemic. The latest figures released Wednesday reveal another dip in net income, down to $1.85 billion - the lowest since Q3 2021. The difference then, though, is that was building on a strong upward trend, not the continuation of a downward one.

Tesla CFO Vaibhav Taneja and CEO Elon Musk ended the Q3 earnings call by touching on the impact of war on consumer sentiment, with Musk saying "buying a new car isn't front of mind" in times like these. Also having an effect on profitability, as detailed in the earnings release, Tesla cites "operating expenses driven by Cybertruck, AI and other R&D projects" as well as upgrades to its factories.