While the economic fallout of the lockdown measures currently taken to contain the COVID-19 pandemic around the world is doubtlessly severe, many experts are hoping that economic activity will return to normal relatively quickly once the virus is contained and countries are opening up again. And while that may be the case, assuming that aid packages prove effective in helping affected businesses and individuals through the lockdown period, one thing will surely remain once the pandemic is contained or a vaccine is found: a mountain of debt.

In late March, U.S. Congress passed a $2.2 trillion aid package to limit the immediate damage inflicted by the lockdown. And while quick relief was certainly necessary to keep businesses afloat and help individuals who just lost their job, the Coronavirus Aid, Relief, and Economic Security (CARES) Act does come with side effects. According to estimates from the Committee for a Responsible Federal Budget, the U.S. budget deficit could soar to a record $3.8 trillion in fiscal 2020, which equals a whopping 18.7 percent of the country’s GDP. Other countries have passed similar aid packages over the past few weeks, leading to soaring debt levels around the world.

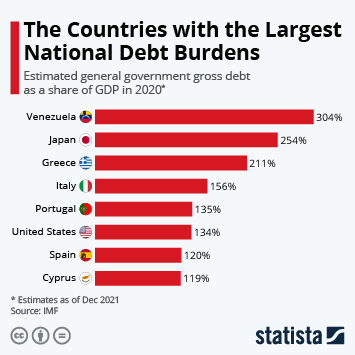

As the following chart based on IMF data shows, debt levels were already very high in many countries before the coronavirus pandemic hit. Take Italy for example, a country that has been hit extremely hard by the outbreak. The Southern European country was struggling with excessive public debt even before COVID-19 shocked the nation to its core, making recovery from the ongoing crisis an even greater challenge. According to the IMF, Germany and China are among the countries better prepared to stomach the additional spending made necessary to keep their economies afloat. Germany in particular has been known for its (widely criticized) austerity in recent years, taking pride in reaching “the black zero”, i.e. a balanced budget for several years.